How do we chart the future of aged care funding and service models in New Zealand?

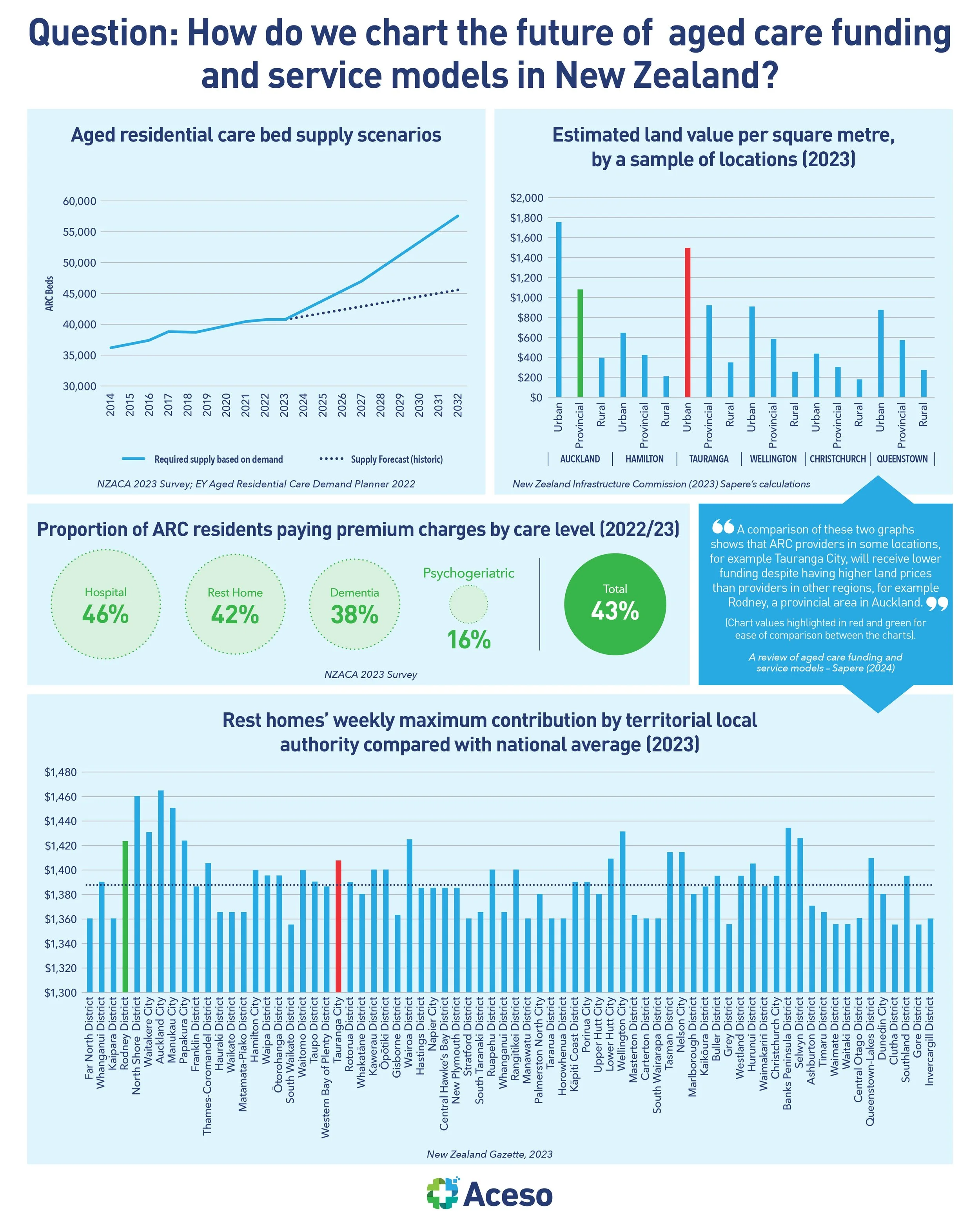

The aged care sector in New Zealand, encompassing aged residential care (ARC) services and home and community support services (HCSS), confronts well-documented challenges that include financial constraints, workforce shortages, and the assurance of equitable access to services. NZ currently hosts approximately 32,000 older individuals in 676 ARC facilities. The majority reside in rest homes (13,500) or in hospital-level care (13,200), while dementia and psychogeriatric units accommodate around 5,500 residents. In the fiscal year 2022/23, Te Whatu Ora allocated approximately $1,352 million to ARC, with residents contributing $1,010 million due to means testing.

A recent Sapere report of NZ’s aged care sector revealed that both the ARC and HCSS sectors are under extreme duress, a situation expected to deteriorate further as the population ages. Forecasts suggest a 33% increase in the number of New Zealanders over 65 within the next decade, rising to more than 280,000. The report warns of a potential shortfall of nearly 12,000 aged residential care beds by 2032 unless significant construction of new facilities occurs. It advocates for substantial investment and a transformative approach to caring for older adults in their homes. The review’s forthcoming second stage aims to propose solutions and evaluate the financial implications and benefits of reforming the current system.

Evidence clearly indicates that the ARC sector suffers from underfunding. The most pronounced underfunding occurs at the rest home level, with a greater funding gap in rural and provincial areas, where providers face challenges in levying premium accommodation charges. The current ARC funding model, differentiated across four care categories, overly relies on an averaged pricing strategy, which insufficiently incentivises proactive management of residents' needs. Data reveal significant disparities in ARC admissions among ethnic groups, with Māori, Pacific, and Asian populations being underrepresented compared to NZ Europeans. Particularly, older Asian populations receive markedly less ARC or HCSS, possibly due to language barriers and issues of social and cultural isolation.

Furthermore, as New Zealand’s population ages rapidly, the HCSS workforce has diminished by 8% in the past two years. ARC providers have noted that the facilities closing are those unable to secure adequate workforce numbers to staff the beds adequately.

The report ends with a note that ARC funding model demands a comprehensive overhaul. The existing scheme, based on broad-based average pricing, fails to adequately incentivise the management of resident needs, disadvantages smaller and regional/rural ARC providers, lacks transparency, and does not align costs with prices effectively.

The question worth pondering over is: how do we fix it and chart a course for the future?